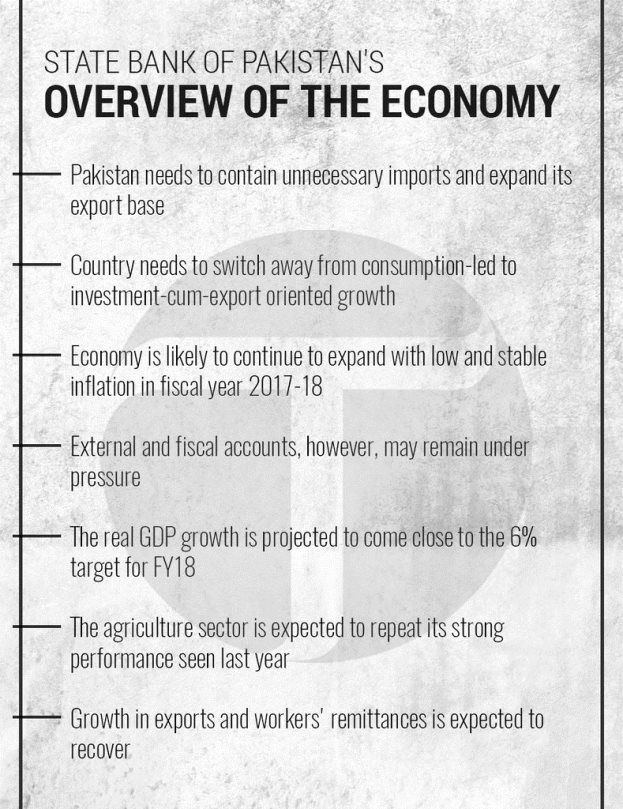

Central bank suggests switch to investment, export-led growth

Report highlights possible pressure on external and fiscal accounts in election year

The current account deficit is projected to remain around last year’s level, ie, in the range of 4% to 5% of gross domestic product (GDP). PHOTO: FILE

The findings are part of the Annual Report on the State of Economy for 2016-17 released by the central bank.

Other notable issues that the report highlighted include switching away from consumption-led to investment-cum-export oriented growth, alleviating credit constraints for small and medium-sized enterprises and enlarging the resource envelope to create the fiscal space required to fund infrastructure and social development projects.

SBP grants banking licence to Bank of China

The SBP assessment shows that the economy is likely to continue to expand with low and stable inflation in fiscal year 2017-18 (FY18).

Encouraging trends in private sector credit indicate underlying dynamics in the real economic activity. However, maintaining this momentum in future would largely depend on addressing emerging challenges in the external and fiscal accounts. The central bank said the latest information presents a mixed picture of macroeconomic conditions in FY18.

The expansion in real economic activity is expected to maintain the momentum and inflation is likely to remain within the target.

External and fiscal accounts, however, may remain under pressure, which is expected to emanate from likely elevated import demand and increase in public spending, by provincial governments in particular, in a bid to complete development projects before upcoming general elections in the country.

The real economic activity is expected to continue benefitting from accommodative macroeconomic policies, activity related to the China-Pakistan Economic Corridor (CPEC) and consistently improving domestic energy supply and security situation. The real GDP growth is projected to come close to the 6% target for FY18.

Agriculture and industry

The agriculture sector is expected to repeat its performance seen last year with major contribution expected from the crop sector, especially cotton and rice.

Notwithstanding a fall in the area under cultivation by 12% against the target, cotton output is expected to remain higher compared to last year. The industry, largely large-scale manufacturing (LSM) sector, construction and electricity generation and electricity and gas distribution will continue to benefit from the ongoing work on infrastructure and energy related to CPEC projects.

SBP introduces new rules to curb terror financing and money laundering

Thus, the expected improved performance of the agriculture and industrial sectors will spill over to the services sector in FY18 as well, the report noted.

With real economic activity gaining further traction, the import demand, both for machinery and raw material as well as consumer goods, is expected to remain strong during FY18 as well.

Remittances and exports

The growth in exports and workers’ remittances is expected to recover. Exports are expected to benefit from a recovery in global commodity prices and ease in energy constraints. This is particularly indicated by a double-digit growth in exports recorded during the first two months of FY18.

In case of workers’ remittances, the initiatives under the Pakistan Remittance Initiative could help in attracting more receipts through official channels.

Key initiatives include new products for the diaspora, extending the tie-up arrangements as practised in the case of Gulf Cooperation Council and the UK to other sources of remittances like Malaysia, South Africa and New Zealand, and plans to further reduce the cost of fund transfers.

With the incorporation of these developments, workers’ remittances are projected to remain in the range of $19-20 billion during FY18.

Yet, the pace of increase in exports and remittances is likely to be slower compared to the increase in imports. Therefore, the current account deficit is projected to remain around last year’s level, ie, in the range of 4% to 5% of gross domestic product (GDP).

The FY18 budget envisages fiscal deficit at 4.1% of GDP. Given the capital spending requirement of the government for completing various projects under CPEC and likely increase in provincial spending during the election year, achieving the 4.1% target could be challenging, the report said.

Notwithstanding expected increase in domestic demand, average Consumer Price Index (CPI) inflation is projected to remain in the range of 4.5% to 5.5% during FY18.

Sufficient food stocks (wheat, rice and sugar), weak domestic oil prices and stable exchange rate are expected to offset the impact of expected rise in domestic demand.

Published in The Express Tribune, October 13th, 2017.

Like Business on Facebook, follow @TribuneBiz on Twitter to stay informed and join in the conversation.

MOST READ

Govt hikes petrol, high-speed diesel prices by Rs26.77 per litre

Foreigner breaches airport security

Gold prices continue to slide in local, global markets

Gold, silver prices rebound in Pakistan after five-day losing streak

FM Araghchi arrives in Islamabad ahead of Witkoff-Kushner visit over weekend for US-Iran talks

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ