Nishat Chunian’s profit jumps 25.5% to Rs3.92b

Earnings per share increases to Rs10.21 in FY17

PHOTO: EXPRESS TRIBUNE

The results were in line with market expectations.

Earnings per share (EPS) jumped to Rs10.21 compared with an EPS of Rs6.85 in the previous year.

The KSE-100 index closed at 42,750, down 24 points or 0.06% on the last trading day of the week. Nishat Chunian’s share price closed at Rs54.56, up 2.5%.

During the fourth quarter, earnings went down by 61% year-on-year or 20% quarter-on-quarter to amount to Rs221 million (EPS of Rs0.92).

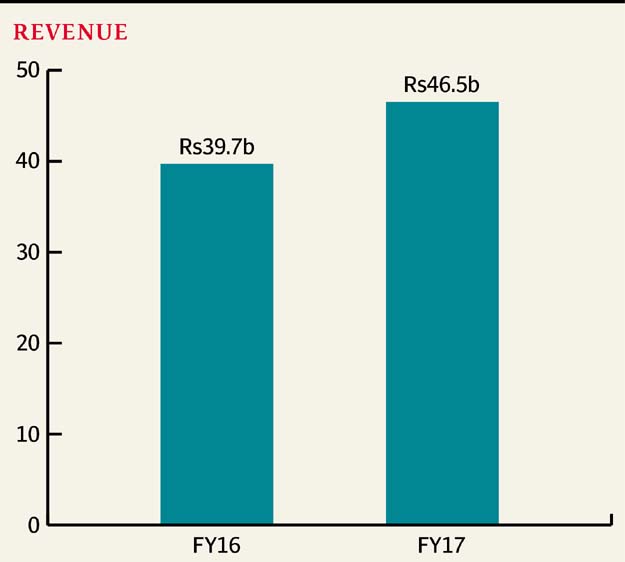

The revenues of the company in fiscal year 2017 settled at Rs46.5 billion, up 17% compared to Rs39.7 billion in the previous year.

Similarly, during the fourth quarter net sales grew up by 14% year-on-year and 2% quarter-on-quarter on account of rebate recorded in the second half of fiscal year 2017, higher sales of fabric and rise in demand of weaving products from Europe along with identification of new markets.

Cost of goods sold stood at Rs38.7 billion during fiscal year 2017 compared to Rs32.9 billion, led by surge in raw material (cotton) prices, which underwent growth of 15% year-on-year along with rising fuel costs up 17% year-on-year. Gross margins of the company eroded by 21 percentage points year-on-year.

Other income for fiscal year 2017 increased to Rs255 million compared to Rs95 million.

Moreover, a meagre decline was witnessed in finance cost during fiscal year 2017, which remained Rs2.24 billion compared to Rs2.26 billion.

Published in The Express Tribune, September 23rd, 2017.

Like Business on Facebook, follow @TribuneBiz on Twitter to stay informed and join in the conversation.

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ