Corporate result: Mughal Iron’s earnings strengthen 11% in FY17

It makes Rs991m profit, declares Rs0.60 per share dividend

PHOTO: REUTERS

The result was in line with market expectations, said a report prepared by Taurus Securities. Earnings per share (EPS) stood at Rs3.94 in FY17 compared with Rs3.55 in the preceding year.

The iron and steel producer announced a final cash dividend of Rs0.60 per share, pushing the entire FY17 pay-out to Rs2.60 per share.

Mughal Iron & Steel profit increases 49%

Mughal Iron’s stock fell 0.70% at Rs61.55 at the PSX. Overall, the KSE 100-share Index closed up 54 points or 0.13% at 42,841 points.

Sales revenue for the company came in at Rs18.8 billion in FY17, down a meagre 1% from Rs19 billion in the previous year despite increase of 5,400 tons in steel production.

The drop in topline was the result of 1.5% year-on-year fall in average sale prices in FY17. Profit margins dipped slightly by 52 basis points to 10.33% because of the lower average sale prices and 12% higher scrap prices year-on-year.

Mughal Steel to invest Rs1 billion for expansion

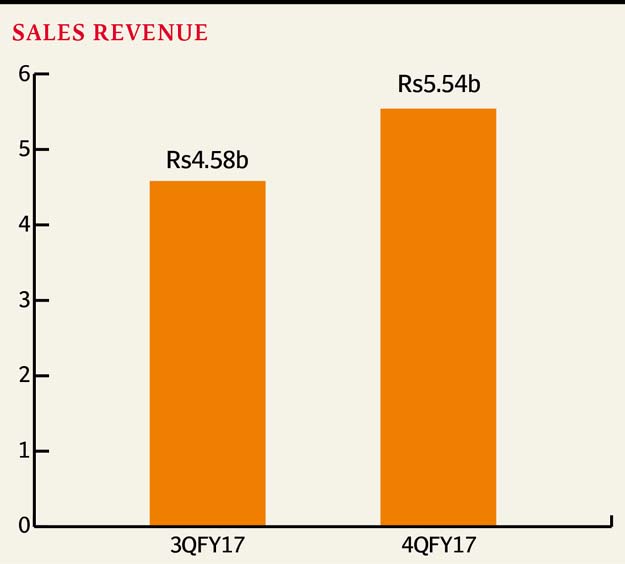

Mughal Iron’s revenues rose 21% quarter-on-quarter following 5% increase in average selling prices quarter-on-quarter and higher steel production as the fourth (April-June) quarter fell in a construction-friendly period.

This translated into net earnings of Rs264 million (EPS Rs1.05) in the fourth quarter, up 4% from the previous quarter.

Published in The Express Tribune, September 19th, 2017.

Like Business on Facebook, follow @TribuneBiz on Twitter to stay informed and join in the conversation.

MOST READ

Apple to manufacture iPhones in Pakistan

Gold, silver prices surge again, local rates hit new highs

Punjab’s quiet acquisition of luxury Gulfstream jet spurs scrutiny

'I like this guy': Trump praises PM Shehbaz, CDF Munir at inaugural 'Board of Peace' summit on Gaza

Imaan Mazari, Hadi Ali Chattha granted bail by ATC in police scuffle case

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ