KAPCO earns Rs9.44b in FY17

Strong income from secondary sources boosts profit

KAPCO. PHOTO: KAPCO

The independent power producer registered a profit of Rs9.07 billion in the preceding fiscal year 2015-16.

Accordingly, earnings per share rose to Rs10.73 in FY17 from Rs10.31 in FY16.

The board of directors recommended a final cash dividend of Rs4.75 per share, taking total dividend payment to Rs9.05 per share in the year, according to brokerage houses.

Resolving issues: Govt urged to address concerns over KAPCO’s privatisation

Kapco’s stock price increased 2.47%, or Rs1.78, to Rs73.65 with 678,000 shares changing hands at the Pakistan Stock Exchange (PSX).

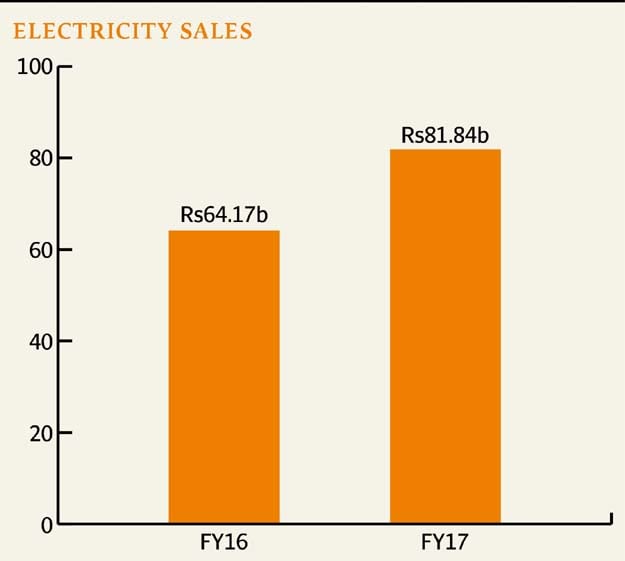

Electricity sales (in rupee terms) surged 28% to Rs81.84 billion from Rs64.17 billion.

“The rise is attributed to higher furnace oil prices (up 29% year-on-year) and higher generation (7,495 gigawatt-hours: load factor 64%), up 14% year-on-year,” Arif Habib Limited said in a post-result analysis.

“The considerable gain in sales failed to fully translate into profit due to higher cost of sales, which rose 33% to Rs67.66 billion from Rs50.77 billion last year,” the report added.

Income from other sources, however, partially extended much-needed support to the power producer in realising higher profit. Other income increased 24% from Rs3.23 billion to Rs4.24 billion.

KAPCO earnings up 38% to Rs2.58b in third quarter

“Other income (likely led by better penal mark-up income) provided partial support to the bottom-line,” said JS Research in a report.

Finance cost surged 37% to Rs4.42 billion from Rs3.23 billion in FY16 due to greater reliance on short-term borrowings, a brokerage house said.

In the last quarter (April-June 2017) alone, profits dropped 8% to Rs2.26 billion (earnings per share Rs2.99) from Rs2.86 billion (EPS Rs3.26) in the corresponding period of FY16.

Published in The Express Tribune, August 23rd, 2017.

Like Business on Facebook, follow @TribuneBiz on Twitter to stay informed and join in the conversation.

LATEST

MOST READ

Kashmiri bangles dominate Eid markets

Govt to absorb Rs49/litre oil price surge

PM Shehbaz says rejected advice to further raise fuel prices, govt to absorb burden

Gold, silver prices fall further in global and local markets

Karachi braces for more rain after morning downpour disrupts Eid celebrations

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ