Profits grew 40% to Rs520 million during the period compared to Rs371 million in the corresponding quarter of 2012

On Monday, Attock Cement – part of Attock Group – announced its performance during the January to March quarter of 2013, which was driven by higher prices of cement during the period despite subdued demand during the winter season.

Profits grew 40% to Rs520 million during the period compared to Rs371 million in the corresponding quarter of 2012, according to a notice sent to the Karachi Stock Exchange.

Yousaf Rahman, analyst at Global Securities, believes that the growth in profitability is attributable to higher cement prices. Cement prices averaged Rs438 per bag against Rs402 in the corresponding quarter of 2012.

Additionally, federal excise duty was reduced by Rs100 per ton during to fiscal 2013 to Rs400, which supported the top-line and bottom-line.

Other contributors included cost reduction due to lower coal prices in the international market coupled with new cost efficient plants. International coal prices averaged $85 per ton in the period under review against $105 per ton during the corresponding preceding quarter, declining by 19%.

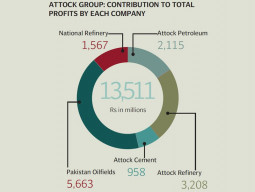

Like most of Pakistan’s construction materials companies, Attock Cement operates just one plant: a 1.8-million ton capacity factory based in Hub, an industrial suburb of Karachi and the only major industrial town in Balochistan.

The producer of the well-known Falcon brand of cements posted a revenue growth of just 9% to Rs3.244 billion in the quarter under review against Rs2.98 billion in the corresponding quarter of 2012, due to lower local and export dispatches, clocking in at 0.37 million tons and 0.13 million tons respectively.

Declining volumetric sales are attributed to lesser funds released for the Public Sector Development Programme during the quarter. During the January to March quarter of 2012 Rs40 billion was released against Rs52 billion in the corresponding quarter of 2012, a decline of 23%.

Gross margins also squeezed to 32% in the period due to increase in company’s fuel and power costs. Though, Attock Cement is trying to cut down its costs as it invested $20 million in setting up a waste-heat recovery plant from which it generates 9.5 megawatts of electricity.

Despite a stellar performance, the announcement was below market consensus attributable to a higher tax rate of 30% levied during the period.

Published in The Express Tribune, April 16th, 2013.

Like Business on Facebook to stay informed and join in the conversation.

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ