SNGPL’s profit jumps 37% to Rs2.6b in Jul-Sept 2018 quarter

Board of directors declares interim cash dividend of Rs1.5 per share

Board of directors declares interim cash dividend of Rs1.5 per share. PHOTO: FILE

The gas marketing company had registered a profit of Rs1.9 billion in the same quarter of previous year, according to a notification of the company sent to the Pakistan Stock Exchange (PSX).

The net profit translated into earnings per share of Rs4.09 in the Jul-Sept 2018 quarter compared to Rs3.03 in the same quarter of previous year.

The board of directors recommended an interim cash dividend of Rs1.5 per share. The entitlement will be paid to the shareholders whose names appear in the register of members on May 15, 2019.

Topline Securities’ analyst Shankar Talreja commented that earnings of SNGPL were higher during 1QFY19 due to the widening of its asset base, as evident from 4QFY18 results.

“Key risks for the company include higher UFG losses, delay in capex (capital expenditure) and regulatory changes,” he said. The cost of gas sales surged 75% to Rs158 billion in the Jul-Sept 2018 quarter compared to Rs90.2 billion in the corresponding period of previous year.

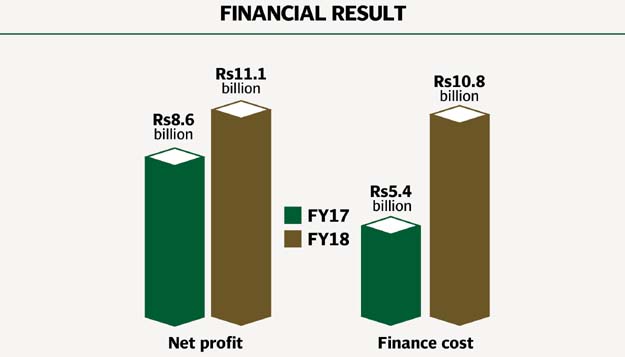

Finance cost increased 155% to Rs4.6 billion in the Jul-Sept quarter compared to Rs1.8 billion last year.

FY18 profit up 29.4%

SNGPL also reported on Monday financial result for the year ended June 30, 2018.

It reported a net profit of Rs11.1 billion (earnings per share Rs17.54) in the year, which was 29.4% higher than Rs8.6 billion (earnings per share Rs13.58) in FY17.

Robust sales, a significant surge in other income and a massive increase in finance cost were the main features of the FY18 result.

The board of directors recommended a final cash dividend of Rs5.55 per share. The entitlement will be paid to the shareholders whose names appear in the register of members on May 15, 2018.

PSO allowed oil import on credit from Azerbaijan

Analyst Shankar Talreja said the higher profit for SNGPL in the fourth quarter of FY18 was the outcome of adjustment of unaccounted-for-gas (UFG) losses retrospectively, contributing Rs1.2 per share to the company’s bottom line.

“To recall, Sui companies were allowed to retrospectively adjust their UFG benchmark to 7.1% for FY13-17 against the actual allowed UFG of 6.73%, 6.91%, 7.08%, 7.14% and 7.11% for the said years. Furthermore, a higher capitalisation of fixed assets during 4Q was also a key reason behind the improved profits.”

Published in The Express Tribune, April 23rd, 2019.

Like Business on Facebook, follow @TribuneBiz on Twitter to stay informed and join in the conversation.

MOST READ

Gold, silver prices drop across global and local markets

IMF loads $7 billion package with 11 new conditions for govt

IMF adds 11 new conditions

Israel, Lebanon to hold second round of talks in Washington on Thursday

New Iran deal 'far better' than Obama nuclear deal, coming 'relatively quickly': Trump

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ