Tax amnesty or NRO for offshore business?

Government should have uniform procedure for all taxpayers

The writer is a former director general of reforms at the FBR and fiscal analyst. He can be reached on Twitter @Chafqat

Is it a genuine step to attract investment or an attempt to give a clean chit at marginal cost is a serious question that needs an objective analysis before it becomes law. Consequently, one needs to figure out what is meant by amnesty and why it is initiated. Also, we need to study its impact on revenue and how it impacts tax culture and lastly will it be open laundered money parked abroad?

To begin with, “A tax amnesty can be defined as a programme that provides for a reduction in real terms of taxpayers’ declared or undeclared tax liabilities as established by law.” (Eric Le Borgne, 2006) Tax amnesties — which are an invitation to tax evaders to join the ranks of people who pay the “unavoidable” taxes — have shown an extraordinary resilience in defaulting on tax liability. When tax authorities can’t catch such chronic evaders and to plug the tax-gap or where tax rates are very high, it offers such schemes. Basically, tax evasion and narrow tax base is due to weak compliance which in turn is a result of several factors, notably (1) weak administration, (2) a weak legal system (or enforcement of the law), and (3) inadequate tax policy. The tax system is too complex with regressive taxes, high tax rates. To address some of these areas, we need to fix the tax system or alternatively adopt out-of-the-box measures.

In different parts of the globe, amnesties are offered. In some developed countries such as France, Germany, England, Italy, the Netherlands, Russia, and Switzerland tax amnesty was introduced in an effort to create tax compliance.

In Latin American countries the authorities experimented but with strong government will. In Asia, India, Indonesia, Malaysia, Pakistan, the Philippines, and Sri Lanka introduced such measures at different times.

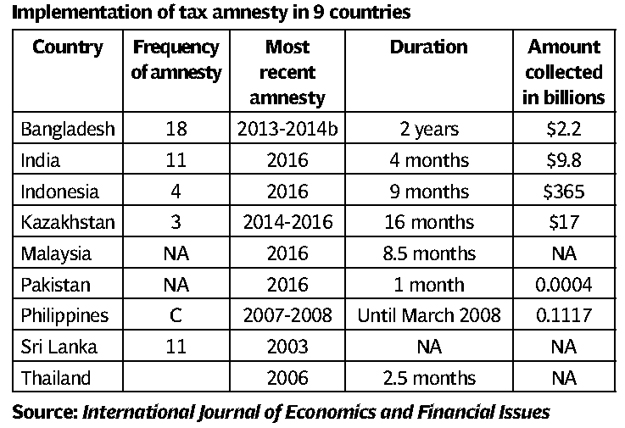

The result of these amnesties in South Asia and East Asia, which is relevant for our analysis, is tabulated below. A cursory look in the table will bring out Indonesia as a success story.

Pakistan has seen mixed outcomes from such amnesties. In 1958, under Field Marshal Ayub Khan, Pakistan’s first tax amnesty scheme brought 71,289 people in the tax net. The new taxpayers declared Rs1.3 billion in assets. In 1969, General Mohammad Yahya Khan’s amnesty added new 19,600 taxpayers with declared assets of Rs920 million. In 1976, Zulfikar Ali Bhutto could collect only Rs270 million through amnesty. In 1986, General Muhammad Ziaul Haq attempted amnesty but met with little or no success. In 1997, then PM Nawaz Sharif could add only Rs141 million through amnesty.

We may also note that in 1998 on appeal by the government rich professionals of Pakistan opened their foreign currency accounts. Then suddenly it took the imprudent step of freezing these accounts fearing capital flight in the wake of Washington suspending aid after Pakistan went nuclear.

In 2000, a campaign was launched for “documentation of the economy” which was a right step but fell prey to the rigidity of the tax machinery. The crucial stage of stock-taking of production was called off as a “referendum overtook this rare time for mainstreaming informal economy. Nevertheless, it resulted in collecting about $3 billion.

In 2016, PM Nawaz Sharif government announced three tax amnesty schemes under which the government expected to bring in a million new taxpayers. But in actual terms only 128 people participated in the scheme.

As stated above, there has been marginal impact upon revenue as well on broadening the tax net under the PML-N regime. Alternative steps should be very exceptional and are to be offered only as one-time relief if the regular tax regime suffers from tax system structural flaws. As we are aware, the CBR/FBR used to waive off surcharges in May and June to meet revenue targets that taxpayers used to default the whole year and would get away with paying the principal amount towards the fag end of years. Secondly, tax compliance bleeds due to political expediency as traders till today are out of the tax ambit as they are seen as a PML-N political constituency. The FBR is prudent enough to lay off its hands. Several ministers and heads of parliament committees are renowned businessmen and always look after their interest. There doesn’t exist any law against ‘conflict of interest’.

The government has made restricted, proposed amnesty to “offshore” business. Its impact has been assessed by AF Ferguson. Its report stated that Pakistanis are holding $150 billion worth of assets abroad out of which $40 billion are invested in foreign real estate. The report also forecast that at best $3 billion to $4.5 billion will be repatriated and the rest will just given a clean chit to loads of people at a very low cost. This is the reason that in safe havens, tax rates are every low and if an offshore company is legally formed why will such a business prefer to relocate to a complex taxation system where tax rates are rather high. And it will tarnish one’s name in case it’s made in the open to offshore companies constituted through laundered money.

Instead of resorting to alternative tax measures, will it not be appropriate to fix the nuts and bolt of taxation systems? Some of the measures that could be introduced include:

1. Simplifying the law and procedures

2. Removing uncertainties and discretionary powers

3. Limiting interaction between the taxpayer and the taxman

4. Reducing tax rates

5. Doing away with unnecessary protection to local industries in a timely fashion

The government should have a uniform procedure for all taxpayers and a significant change such as tax amnesty should be made subject to approval of the Council of Common Interests, a statutory body of the federating units. Lastly, it would be beyond the mandate of the current government to offer any serious scheme towards the fag end of its tenure. The abiding principle for any effective tax system is to let it override political expediencies.

Published in The Express Tribune, February 4th, 2018.

Like Opinion & Editorial on Facebook, follow @ETOpEd on Twitter to receive all updates on all our daily pieces.

MOST READ

Pak pilgrims slam Hajj arrangements

Industrial estate approved along Rawalpindi Ring Road

FY27 budget may offer limited relief

Trump says US not satisfied yet on deal with Iran

Pak-China friendship will grow broader like Karakoram Highway

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ