Private financing up by 7.4%

Growth in bank advances, drop in deposits helped them avoid additional taxes

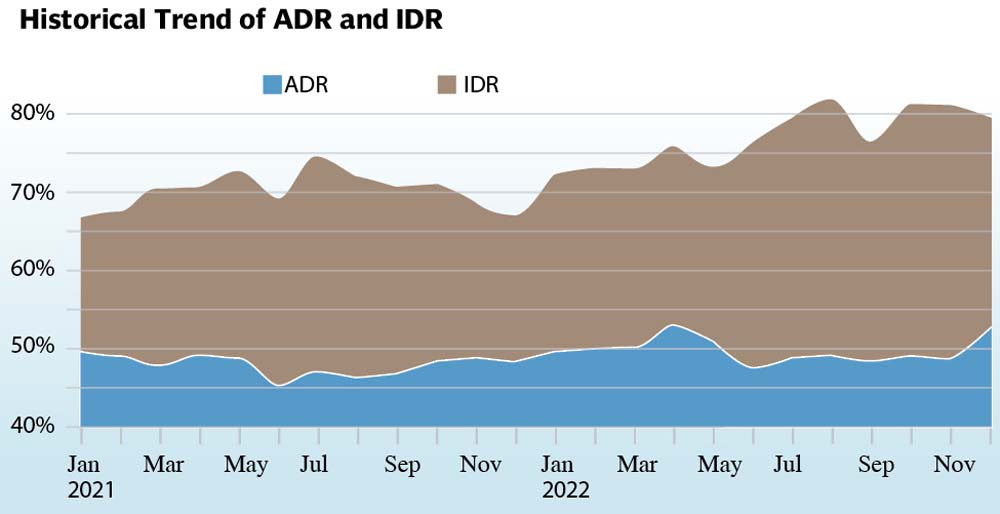

Banks have exhibited a surprisingly notable growth of 7.4% in financing to the private sector (called advances) rising to Rs11.91 trillion at a time when businesses are closing operations due to economic hardship in the country.

They did, however, report a drop of 1.2% in deposits to Rs22.46 trillion in December, compared to Rs22.73 trillion in November.

The reported growth in advances and drop in deposits; both helped the banks to achieve the assigned target of advance-to-deposit-ratio (ADR) of 50%. A slippage in ADR below 50% would have forced the banks to pay additional taxes, which they managed to avoid by apparent number juggling.

Arif Habib Limited’s Economist Sana Tawfik remarked that it is surprising to note the deposits have dropped in December. “December used to be a month of war among banks. Each one would be fighting to attract the maximum number of deposits to close their books at high deposits. The drop, however, suggests they have (intentionally) avoided accepting new deposits this December to achieve compliance with the 50% ADR.”

The data suggests that ADR increased 4.23 percentage points to 53% in December 2022, compared to 48.8% in November 2022. A growth in deposits would have led towards slippage in ADR below 50%.

“It is also surprising to note that banks have extended new loans worth around Rs800 billion (or 7.4%) to the private sector in the single month of December, as a large number of businesses have been reporting partial or complete closure due to the non-availability of imported raw material for the past couple of months,” she stated.

The breakup of the data, when reported later in the days to come, will reveal details about those who have taken the loans, and for what purpose, during these testing times, she said.

The government stands to be the single largest borrower from commercial banks these days and its borrowing is not classified in the category of advances (credit to the private sector).

Throughout 2022, the banks kept their complete focus on making the maximum lending to the government. Such financing remains risk-free lending as the government never defaults on its repayments. Banks provide financing to the government by investing in sovereign debt securities like T-bills and Pakistan Investment Banks (PIBs). That’s why they classify their lending to the government as an “investment”.

The data also suggests banks’ investments in government debt securities increased by almost 27% in the previous year, reaching Rs17.90 trillion in December 2022, compared to Rs14.12 trillion in December 2021.

Accordingly, their investment-to-deposit ratio soared by 12.33 percentage points to 80% in December 2022, compared to 67% in December 2021.

The government’s reliance on domestic debt went up in 2022 due to a significant drop in foreign financing in the year. The government mostly takes lending from commercial banks, as taking loans from the central bank to finance its fiscal deficit is prohibited.

The deposits have increased by 7% through the previous year to Rs22.46 trillion in December 2022, compared to Rs20.97 trillion in December 2021.

The growth in deposits has been marked mainly due to a receipt of workers’ remittance sent home by overseas Pakistanis, said Tawfik.

A notable surge in the government’s borrowing itself remained a major source of growth in deposits for the banks, she said.

The advances surged by 17.4% through the year to Rs11.91 trillion in December 2022, compared to Rs11.09 trillion in December 2021. “A notable surge in car financing in the initial months of 2022 remained a leading reason behind the growth in advances in the year. Car financing, however, dropped significantly in the last months of the year (including in December 2022),” she noted.

Meanwhile, the Pakistani currency maintained a downward streak, rising beyond Rs228 against the US dollar in the interbank market, after a gap of over three-months on Thursday.

The local currency shed a fresh 0.09% (or Rs0.21) to an over three-month new low at Rs228.14 against the greenback. The revival of the International Monetary Fund’s loan programme has become a major pain-point for the currency, resulting in its constant downtick.

The rupee may face extended pressure against the foreign currency after the central bank reported the country’s foreign exchange reserves to have fallen by an additional $1.23 billion, bringing to a nine-year low at $4.34 billion. The reserves are barely enough for a three-week import cover.

It is believed that the announcements like the UAE rolling over its $2 billion loan and providing another $1 billion in deposits to the State Bank of Pakistan (SBP) will help offset the negative impact of the drop in the reserves.

Saudi Arabia’s announcement to extend a credit line of $1 billion for the import of oil over the next one-year will also improve the weak reserves.

Published in The Express Tribune, January 13th, 2023.

Like Business on Facebook, follow @TribuneBiz on Twitter to stay informed and join in the conversation.

LATEST

MOST READ

PM Shehbaz approves Rs32.12 per litre cut in high-speed diesel price

Govt abolishes free electricity units facility for power sector employees

Pakistan sets the stage for next round of talks

PM seeks relaxation in honorarium policy

Govt overhauls civil service conduct rules

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ