Debt, liabilities jump to Rs44.8tr

Pace of debt accumulation in the country slows down significantly

Pakistan’s debt and liabilities peaked to a record Rs44.8 trillion at the end of September this year, an addition of Rs3.3 trillion in a year, but the pace of debt accumulation slowed down significantly, reported the State Bank of Pakistan (SBP) on Wednesday.

The release of latest debt bulletin by the central bank coincided with the International Monetary Fund’s (IMF) executive board discussion to propose new global reforms for public debt policy aimed at bringing transparency and tailoring conditions of concessional loans being received by different countries.

Statistics released by the SBP showed that by September this year, the country’s total debt and liabilities soared to Rs44.8 trillion. There was an increase of Rs3.3 trillion or 7.9% in the overall debt and liabilities. It was one of the slowest rates of increase in the debt during Pakistan Tehreek-e-Insaf’s (PTI) tenure.

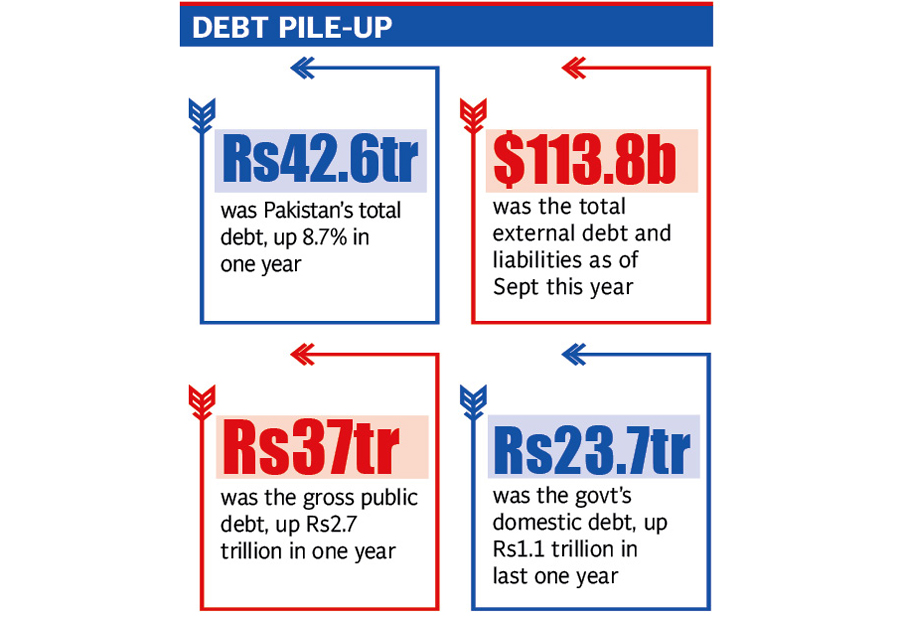

The Rs44.8-trillion debt and liabilities were equal to 98.3% of current fiscal year’s projected gross domestic product (GDP) of Rs45.6 trillion. Excluding the liabilities, the country’s total debt swelled to Rs42.6 trillion, up Rs3.4 trillion or 8.7% in one year.

Total debt and liabilities also include the public sector enterprises’ (PSEs) debt, non-governmental external debt and inter-company external debt from direct investors abroad.

The IMF executive board also reviewed the Fund’s policy on public debt. An IMF statement noted that while public debt vulnerabilities had risen sharply outside of IMF-supported programmes, they had been contained within IMF-supported programmes.

It said that still substantial challenges to the current debt limit policy were present in several areas.

These areas are migration of debt-related risks off balance sheet; problems with debt transparency; tighter-than-anticipated policy implementation in countries normally relying on concessional financing; and a poor fit for countries that normally rely on concessional financing but have recently started accessing international financial markets on a significant scale, where debt conditionality is not well aligned with their new credit landscape.

The IMF proposed that there should be adequate debt disclosures to the IMF; and the countries should allow for greater tailouring of debt conditionality for countries normally relying on concessional financing that have also been accessing international financial markets.

Pakistan made certain changes in its debt definition a couple of years ago and shifted the Chinese debt from the central bank’s balance sheet to the federal government to satisfy the IMF. However, still certain Chinese financial assistance remains on the central bank balance sheet.

The SBP said on Wednesday that external debt and liabilities of Pakistan mounted to $113.8 billion as of September this year. In the past one year, a net $6.8 billion was added to the external debt and liabilities by the federal government, SBP and private sector.

Total external debt and liabilities surged to Rs18.9 trillion on the back of currency depreciation during first two years of the ruling party and new borrowing.

The debt taken by Pakistan from the IMF increased in rupee terms by Rs268 billion to Rs1.26 trillion.

After coming to power, the PTI government had started devaluing the local currency but the rupee has now again started appreciating, which will lower the external public debt in rupee terms.

The central bank’s decision to keep interest rate high at 13.25% till March this year also adversely affected fiscal operations of the federal government. Of the Rs44.8 trillion, the gross public debt, which was the direct responsibility of the government, increased to nearly Rs37 trillion as of the end of September, said the SBP.

The gross public debt was now equal to 81.1% of GDP, far higher than the 60% statutory limit set in the Fiscal Responsibility and Debt Limitation Act of 2005. There was an increase of Rs2.7 trillion in the gross public debt in one year.

The government’s domestic debt surged to Rs23.7 trillion with the addition of Rs1.1 trillion in the past one year. Its external debt increased to a record Rs12 trillion.

Total liabilities, which were indirectly the responsibility of the finance ministry, slightly decreased to Rs2.25 trillion. There was a reduction of Rs109 billion in the liabilities. Domestic liabilities increased from Rs741 billion to Rs753 billion. But external liabilities dropped from Rs1.6 trillion to Rs1.5 trillion in one year.

Interest payments on debt and liabilities increased to Rs759 billion in the first quarter of current fiscal year, which was higher by 39%.

Domestic interest payments on debt stood at Rs661 billion, an increase of Rs235 billion or 55%. External debt interest payments fell to Rs98 billion in the first quarter.

“We are in a debt trap that is entirely of our own making. It is a risk to our national security,” said a brief report of the Institute of Policy Reforms (IPR) last month.

The IPR paper underlined that the government was borrowing to repay the maturing debt.

Published in The Express Tribune, November 12th, 2020.

Like Business on Facebook, follow @TribuneBiz on Twitter to stay informed and join in the conversation.

MOST READ

PMD predicts rain, thunderstorms in parts of Sindh

Severe heat persists in Sindh as Karachi records humid conditions

Iranian negotiator says final draft not yet approved, Tehran can quit US deal over violations

Gold prices rise in local, global markets

Trump announces end of Iran naval blockade, says now making 'final determination' on deal

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ