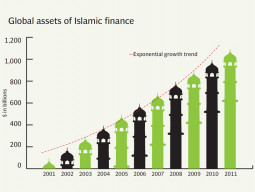

Interest-free and subject to high moral codes, growth will be slow in the long-run. SOURCE: QUARTERLY UNAUDITED ACCOUNTS

KARACHI:

While Islamic financial institutions have passed the robustness test by exhibiting greater resilience during the recent global financial crisis, the crisis has also brought under the spotlight some important challenges the industry is currently facing. Going forward, the stakeholders of Islamic finance will need to address a broad spectrum of issues surrounding the industry.

Highlighting the inherent strengths of Islamic finance, the recent global financial crisis coincided with the growing concerns over the possibility that excessive financial innovation might lead the Islamic finance products to bend certain key precepts of Muslim jurisprudence to breaking point. Perhaps the most prominent example is the Sukuk – sometimes even called the “Islamic bond” – as many Islamic Sukuks have gone too far in mimicking conventional, interest-bearing bonds, which are prohibited in Islam.

Diversifying assets

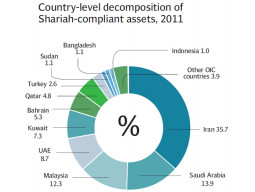

Since there is little room for diversification of assets, the risk management capabilities of the Islamic financial institutions are limited. A direct consequence of this was observed in the last financial crisis when large exposure to real estate of Islamic financial institutions resulted in falling asset values in many of these institutions operating in the OIC member countries, particularly in the MENA region. A study by Ernst & Young (2011) reveals that the real estate concentration still remains a concern for Islamic finance industry and may affect its future growth.

The low penetration levels of Takaful (Islamic insurance) in OIC countries are posing another challenge for the Islamic finance industry. OIC member countries as key Takaful markets are characterised by low insurance penetration rates versus huge potential for rapid economic growth. Global Takaful premiums are estimated by Ernst & Young (2011b) to have reached $16.5 billion in 2011. Moreover, Takaful premiums remain highly concentrated in Iran which generated almost 30% of the global Takaful premiums in 2011. Similar to the relative size of Islamic finance to the global financial industry, the Takaful market represents only 1% of the global insurance market at present (Ernst & Young 2011c).

Regulation and standardisation

Another major impediment to the growth of Islamic finance industry is the weak Islamic finance enabling infrastructure in many OIC countries. Enabling infrastructure would include, among others, legislative, regulatory, legal, accounting, tax, human capital, and Shariah business frameworks. Although member countries such as Bahrain, Malaysia and UAE are among the major Islamic finance centres with developed infrastructures, in many others, an enabling environment is not in place. This, in turn, increases operational risks, including the risk of Shariah compliance.

Development of Islamic money and capital markets, provision of standardised liquidity management tools, improvement of the operational efficiencies of Islamic financial institutions, standardisation in products, synchronisation of regulatory frameworks, and human capital accumulation are other areas where the Islamic finance industry needs to take structural steps.

Broadening the skill base

The broadening of the global skills base in Islamic finance is desirable since the number of qualified practitioners, as well as Shariah scholars available for Shariah boards, is currently very low.

Representation of Shariah scholars on Shariah boards is highly concentrated. A survey by Funds@Work (2011) reveals that only the top 20 Shariah scholars hold 619 board positions which represent more than half of the 1,141 positions available.

All in all, with the challenges ahead, the growth of Islamic finance, free from interest and subject to high moral codes, will be slow in the long-run. And the slow growth of the industry would also slow down economic growth and wealth creation. However, the wealth created would be real, more equitably and profitably distributed, and would encourage spin-offs into real economy, creating jobs, increasing trade both domestically and internationally.

Published in The Express Tribune, April 22nd, 2013.

Like Business on Facebook to stay informed and join in the conversation.

COMMENTS

Comments are moderated and generally will be posted if they are on-topic and not abusive.

For more information, please see our Comments FAQ